February 2026

Energy

Libya

Nearly a year Nearly a year after Libya launched its first licensing round since 2007, offering 22 onshore and offshore blocks and attracting interest from 44 companies and one consortium, only two offshore and three onshore blocks were ultimately awarded in February 2026.

What this means…

The March 2025 licensing round was intended to signal Libya’s upstream comeback after more than a decade of political uncertainty. The strong early participation suggested renewed investor willingness to re-engage, supported by recovering oil production and relative stability.

However, of the 45 entities that initially indicated interest, 37 advanced through the pre-qualification stage, yet more than two dozen ultimately did not submit final bids. In the end, only five blocks were awarded; onshore Block S4 was granted to Chevron, onshore Block C3 awarded to a consortium comprising Repsol and Turkish Petroleum Corporation (TPAO), alongside offshore Block O7 with MOL Group, offshore Block O1 awarded to a joint venture between Eni and QatarEnergy, and while onshore Block M1 awarded to Aiteo.

The disparity between early enthusiasm and final participation raises legitimate concerns about investor confidence. While the March 2025 bid round initially conveyed a sense of improving stability, we speculate that subsequent security developments may have dampened investor confidence. Just two months after the bid round was launched, clashes erupted in Tripoli between the 444th Combat Brigade, a state-funded military unit, and the Stability Support Apparatus, a militia group. The incident renewed concerns about the persistence of security risks and political instability in the region. These factors continue to weigh heavily on long-term investment decisions.

Source: https://oilprice.com/Energy/Energy-General/Libyas-Oil-Licensing-Round-Fails-to-Deliver-Promised-Comeback.html

Agriculture

Nigeria

1) The Board of the African Development Bank Group has approved a $200 million loan to support the second phase of Nigeria’s National Agricultural Growth Scheme. The financing will enhance productivity, strengthen value chains, and accelerate the adoption of climate-smart, data-driven farming practices.

Our thoughts…

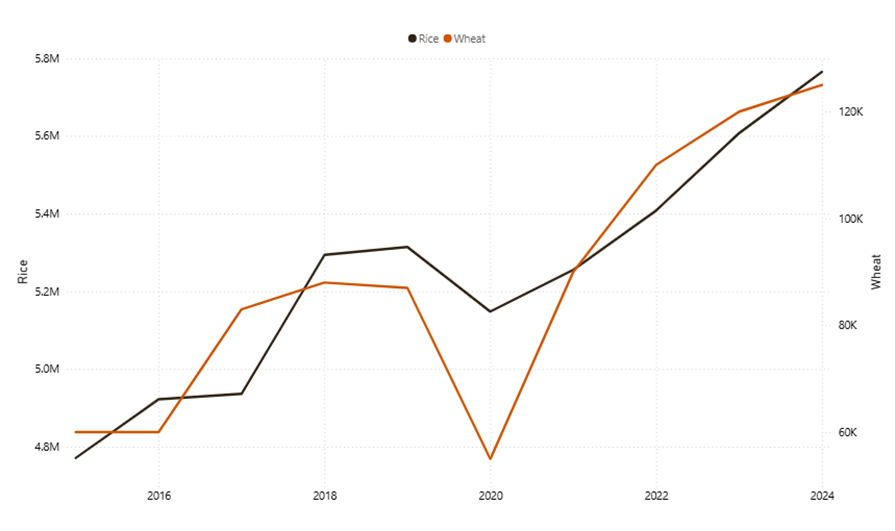

The first phase of the programme, launched in 2023 with a $134 million loan from the African Development Bank Group, focused primarily on boosting year-round grain production. Central to the initiative were targets to increase wheat production fivefold and raise rice output by 20%. However, data from the United States Department of Agriculture indicates that wheat production increased 4.17%, while rice output rose by only 2.82% between 2023 and 2024, far below the projected targets of 500% and 20% respectively. Moreover, these figures represent declines of 5% for wheat and 1% for rice compared to the previous year. Preliminary assessments suggest that agroclimatic challenges and heightened insecurity, particularly in northern regions, may have undermined the programme’s performance during the first phase.

Phase Two, which commenced in March 2026 and is scheduled to run for four years, reflects a shift from production expansion alone to strengthening the wider agricultural ecosystem. Among its five priority pillars is the promotion of digital and climate-smart agriculture, likely introduced in response to the environmental and operational challenges encountered in the first phase. Additional focus areas include improved access to quality seeds, revitalised agricultural extension services, enhanced agricultural data systems, and stronger value chains for staple crops.

Source: https://www.afdb.org/en/news-and-events/press-releases/nigeria-african-development-bank-group-approves-200-million-boost-agricultural-production-and-reduce-food-imports-90885

Fig 1: Wheat and rice production in Nigeria, 2015-2024

Source: USDA FAS— Nigeria

2) Nigeria’s federal government has begun the rollout of 2000 tractors and 9000 agricultural implements seven months after launching, to promote mechanized farming across the country under the Renewed Hope National Agricultural Mechanization Programme (RHAMP).

Our thoughts…

Since the 1970s, the federal government has introduced a range of policies and programmes aimed at promoting agricultural mechanization across the country. A recurring strategy in these initiatives has been to provide farm machinery to private owners and mechanization service providers at subsidized rates, with the expectation that smallholder farmers would gain access to these machines through affordable hiring arrangements. In principle, this model is sound. In practice, however, the scale of implementation has been far from adequate.

Current estimates indicate that fewer than 45,000 functional tractors are available for agricultural use nationwide as of 2024, even when accounting for contributions from state governments and the private sector. When placed in a global context, this figure highlights a significant deficit. Germany, for instance, with approximately 11.8 million hectares of arable land, operates more than two million tractors. Nigeria, which has about 36.9 million hectares of arable land, over three times Germany’s total, would theoretically require about 6 million tractors to achieve comparable mechanization levels.

Source: https://allafrica.com/stories/202602170114.html

South Africa

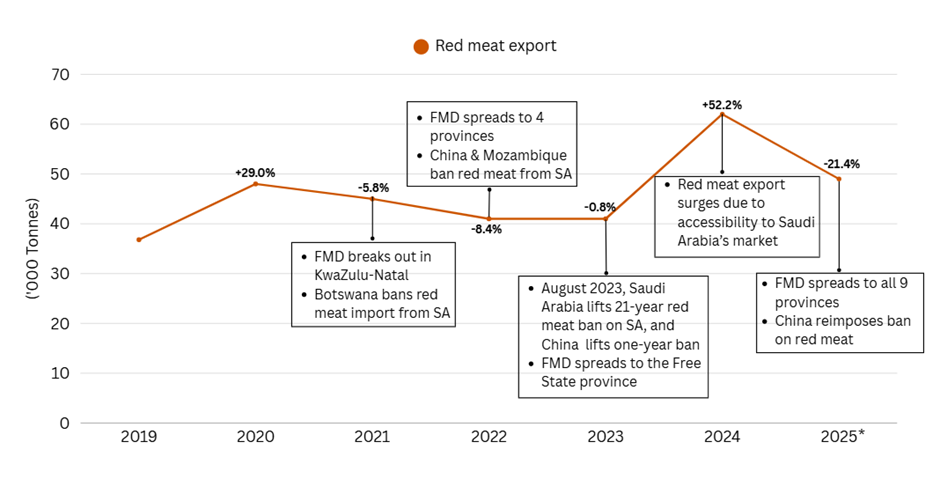

Five years after the most devastating foot-and-mouth disease (FMD) outbreak started in KwaZulu-Natal, the Ministry of Agriculture has received one million doses of FMD vaccine to augment local production and strengthen containment efforts. Sources report that five million doses would be delivered by the end of March.

To provide context…

The current outbreak, which began in 2021, has spread across herds in all nine provinces and has become the most severe outbreak in recent history. In 2025, it resulted in an estimated $352.2 million loss in export revenue, severely impacting the livestock (cattle, sheep, goats, and pigs) sector.

As livestock quality and quantity continue to decline, South African consumers are bearing the brunt through rising meat prices. At the same time, export bans imposed by Zambia, Mozambique, Zimbabwe, Namibia, Botswana, Democratic Republic of Congo, and China have further strained the national economy. Farmers’ livelihoods have also been significantly threatened, emerging as another major pressure point in the crisis.

All countries bordering South Africa, except Namibia, have reported one or more strains of the disease, raising concerns about regional containment and cross-border transmission.

Source: https://www.gov.za/news/media-statements/minister-john-steenhuisen-arrival-one-million-fmd-vaccine-doses-argentina-17

Fig 2: South Africa’s red meat export, 2019-2025

Source: https://trademap.org, Moneda intelligence

*- Not the full year

Mining & Construction

Zimbabwe

The Ministry of Mines and Mining Development has placed an immediate ban on the export of all raw minerals and lithium concentrates, including shipments currently in transit. Exempting only mining companies with valid titles and approved beneficiation plants.

What this means…

Zimbabwe has joined the growing list of African countries; Ghana, Namibia, Malawi, Tanzania and Nigeria that have banned the export of raw minerals. Outcomes from similar policy suggest that this restriction can be effective in attracting foreign investment. For instance, Nigeria’s foreign direct investment in the mining sector increased by 700%, from about $100 million in 2022 to over $800 million in 2024, following the ban on raw mineral exports introduced in the final quarter of 2022. Tanzania has recorded even stronger momentum, attracting $10.95 billion in mining investments in 2025 alone.

Zimbabwe’s policy carries broader global implications due to its strategic position in the lithium market. As the world’s fourth-largest lithium producer, accounting for more than 9% of global output, the export restriction has raised concerns about potential supply disruptions. This comes at a time when rising expectations for energy storage systems have already driven an uptrend in lithium prices since June 2025, according to Reuters. Zimbabwe is also a key supplier to China, accounting for an estimated 15–19% of the country’s lithium concentrate imports in 2025. Following the policy announcement, lithium carbonate, a key derivative of lithium concentrate recorded an immediate market reaction, with prices rising by about 6% on the Guangzhou Futures Exchange.

Beyond its immediate market impact, the move signals the government’s intention to tighten oversight of the mining industry and encourage investment in local processing and refining facilities, enabling the country to capture a greater share of the lithium value chain. Thereby positioning itself to shift from exporting low-value feedstock to developing a more value-added domestic mining and manufacturing industry.

Leave a Reply