March 2026

Energy

The Strait of Hormuz Ripple Effect

The Strait of Hormuz, a passage that lies within the territorial waters of Iran and Oman, was at the center of global attention during the month of March. It is one of the world’s most critical energy corridors as it provides passage for about 20% of global LNG trade and 25% of global seaborne oil trade. Escalating conflict between the U.S and Iran following missile attacks to critical infrastructure has forced Iran to mount a blockade on the Strait preventing the safe passage of oil and gas tankers through it. Traffic through the strait dropped by about 30% in the month of March, raising crude oil prices by 61%.

With respect to energy security, neither party to the conflict has felt much adverse effect, but the rest of the world has been collateral damage. For our March 2026 recap, Moneda Intelligence analyzes how the lack of sovereignty that exists in Africa’s energy industry exposes it to global shocks like the Strait of Hormuz.

The gas plague of Egypt

Once strengthened by the Zohr discovery, a giant gas field with 30 trillion cubic feet in reserves, Egypt’s strength turned to weakness almost overnight due to a sharp decline in production from the field. The country quietly shifted from gas exporter to an importer following a $35 billion natural gas supply deal with Israel in 2025 which was expected to run till 2040.

Following this reality, the impact of the Strait of Hormuz is closing in on Egypt in three fronts:

- Only a few months after its landmark deal, Israel is forced to cut off supplies to Egypt leaving power plants without adequate gas to meet power demand.

- There has been a significant shrinkage in foreign trade as the country also cut off its gas transshipment to Europe, Jordan and Lebanon due to its own lack of supplies from Israel.

- The pump price of gasoline in the country has surged by 14.3% due to a reliance on imports.

The combination of these three effects has forced Egyptians to close shops, restaurants, tourist centers and government offices earlier and reduced street lighting.

Source: Egypt energy-saving method

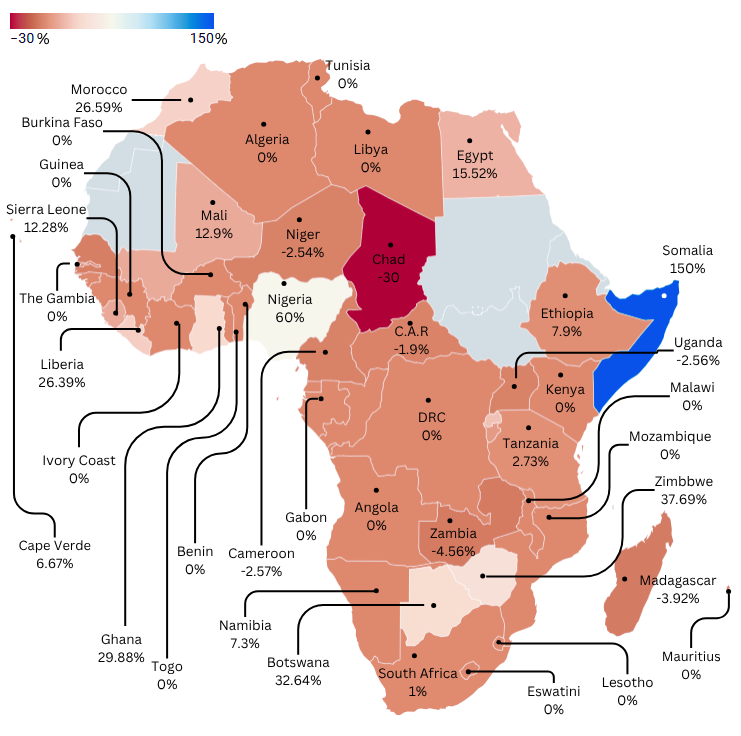

Fig 1: Percentage change in petrol price across Africa, February 23rd, 2026 – March 31st, 2026

Source: Moneda intelligence

Fuel price increases emerged as a direct consequence of disruptions along the Strait of Hormuz, but the impact varied significantly across countries. While some absorbed severe shocks, others implemented strategies to cushion the effect, and a few operated under entirely different market conditions.

Across 48 African countries analyzed between February 23 and March 31, the divergence is clear. About 37.5% recorded price increases, 45.83% remained stable, and 16.67% experienced declines.

Somalia recorded the steepest increase at 150%, particularly in Mogadishu. The surge reflects the country’s highly liberalized fuel market, where importers directly pass rising costs, ranging from higher import prices to increased insurance premiums for tankers navigating the Red Sea and Gulf of Aden, onto consumers. The situation is further compounded by the absence of domestic crude production or refining capacity, alongside prolonged instability.

Nigeria followed with a 60% increase, despite being one of Africa’s top oil producers and home to a 650,000-bpd refinery. Price movements were swift, with a 10% increase recorded within a day between February 27 and 28, followed by continued volatility in line with global crude prices. This outcome reflects ongoing reliance on imported refined products, exposure to high-cost crude imports, and the absence of price buffers following subsidy removal in 2023. In contrast, countries such as Congo Brazzaville, Tunisia, Gambia, Gabon, and Equatorial Guinea maintained more stable pricing through regulated markets and structured monthly adjustments by regulatory authorities.

Morocco and Zimbabwe illustrate a different pattern, where price increases occurred in multiple phases rather than immediately. Morocco adjusted prices four times within the period, while Zimbabwe recorded two separate increases, suggesting initial pricing levels were insufficient to absorb sustained global pressures.

Benin Republic presents a dual-market dynamic. Official fuel prices, unchanged since January 1, 2025, remained stable, while informally traded fuel, largely sourced from Nigeria and sold roadside rose by about 50%. This is notable given that the same fuel was previously priced at about 28% below official rates.

Madagascar and Chad stand out among countries that recorded price declines, though at the cost of supply shortages. Chad, despite a 30% drop in official fuel prices, faced significant scarcity, pushing consumers toward the black market where prices were approximately 26% higher than official levels.

The overall pattern reinforces a key theme: beyond global price movements, domestic market structure and policy responses play a decisive role in determining how fuel shocks are transmitted to end users.

Libya

In a period of tightened global oil supplies, Libya announced the restart of four critical oil infrastructure injecting 415,000 barrels of oil per day back into the market.

On March 12, 2026, TotalEnergies announced the restart of production at the Mabruk oil field, an onshore asset that has been offline since 2015 due to security disruptions. This follows the development of a new production unit with a capacity of 25,000 barrels per day, launched in May 2024 and brought online on February 28, 2026.

Less than a week later, on March 17, 2026, a fire broke out at the Sharara oilfield, one of Libya’s largest with capacity of about 300,000bpd caused by a valve leak. Crude oil exports were not initially impacted as an alternative evacuation route was activated through the El Feel pipeline. However, the discovery of exploded projectiles near a damaged section of the Sharara pipeline triggered the shutdown of both Sharara and El Feel. Crude supplies were only impacted for the period of the shutdown, which lasted about a week before the completion of maintenance work.

Finally, the Al-Sarir refinery resumed operations in March after nearly three years offline due to political tensions surrounding the leadership of Libya’s central bank. This comes after the Arabian Gulf Oil Company completed a major overhaul of its Crude Distillation Unit. Al-Sarir is Libya’s fifth largest refinery and can process about 10,000 bpd of crude per day. The combined effect of the restart of these facilities is a paradox – Libya has long been defined by instability and uncertainty that have impacted supplies but, in a period, where the rest of the continent grapples with fuel shortages, Libya experienced an increase in supplies.

Sources: Mabruk Oil Field, Sharara and El Feel Oilfield

Angola

Angola holds an estimated 343 billion cubic meters (bcm) of natural gas reserves and ranks as the 5th largest gas producer in Africa, with current production of about 5.5 bcm, just 1.61% of its total reserves. However, most of this output is still derived from associated gas tied to oil production.

On March 17, TotalEnergies announced the start of production of the Quiluma-Maboqueiro gas project, Angola’s first major non-associated gas development. The $2.4 billion project, at peak output, is expected to produce about 3.41 bcm annually, lifting Angola’s total gas production by roughly 62%. The development forms part of the New Gas Consortium (NGC), a broader effort aimed at unlocking standalone gas resources and reducing reliance on oil-linked production.

The gas from Quiluma-Maboqueiro will be processed and transported via a new 100km subsea pipeline to the Angola LNG facility through a new 100km subsea pipeline to the processing plant in Soyo before it is exported, with a portion reserved for domestic consumption. The project brings together a consortium of international and domestic players, including BP and Eni in a 50:50 joint venture, Cabinda Gulf Oil Company (Chevron’s subsidiary in Angola), TotalEnergies, and the state-owned Sonangol E&P. Notably, the project reached Final Investment Decision in 2022 and is on track for its stipulated first production in 2026 which has begun, reflecting a relatively disciplined execution timeline compared to many large-scale energy developments across the continent

Agriculture

Nigeria

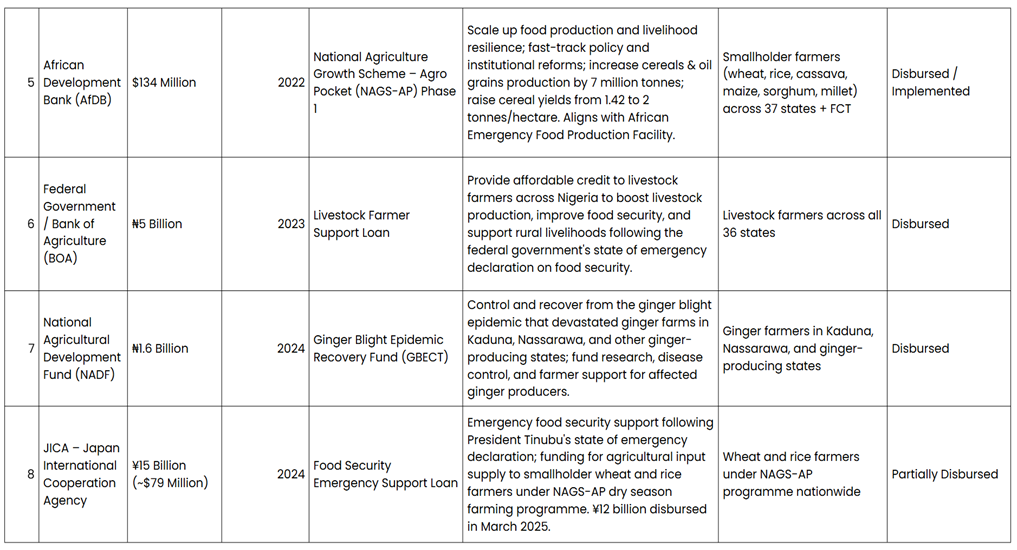

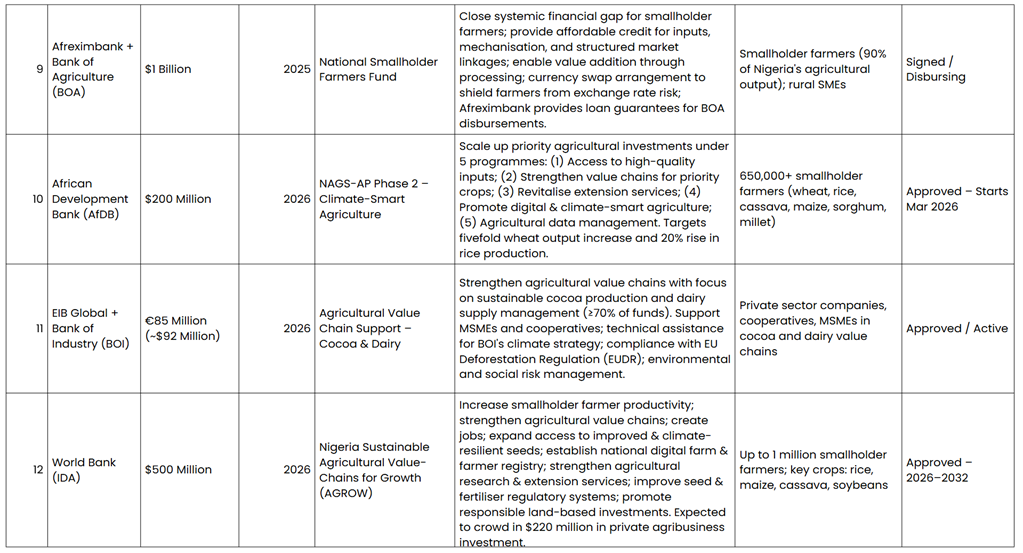

The World Bank, through its International Development Association (IDA), has approved a $500 million loan to boost Nigeria’s agricultural productivity, strengthen value chains, and improve food security under the Nigeria Sustainable Agricultural Value-Chains for Growth (AGROW) project.

Another big funding headline, but what does it really say?

IDA financing is designed for the world’s poorest countries, offering highly concessional terms, little to no interest, repayment periods of 30–40 years, and grace periods that can stretch up to 10 years. The World Bank classifies Nigeria as a “blend” which means it can access both concessional and non-concessional funding, however the country has largely relied on concessional terms. Nigeria has accessed facilities in excess of US$20 billion from the IDA over the last 10 years with US$11.1 billion already disbursed. Nigeria’s agricultural sector has been one of the biggest recipients of these loans and this recent loan approval is not different – Project AGROW targets growth in key crops like rice, maize, cassava, soybeans, yam, and tomato by supporting smallholders with better input, technology, and market access. Just last month, the African Development Bank also approved a similar loan to Nigeria valued at $200 million. While the rising food insecurity provides a strong basis for these loans, despite these commitments from multilateral organizations, the industry is still largely driven by smallholder farmers using traditional methods.

Source:https://nairametrics.com/2026/04/02/world-bank-approves-500-million-loan-for-nigerias-agriculture-sector/

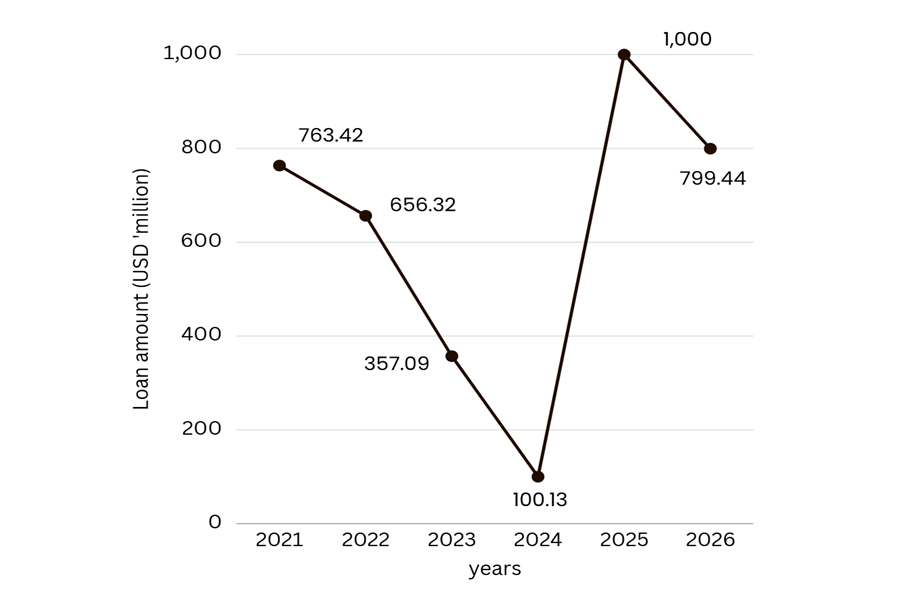

Fig 2: Approved Loans for the Agricultural Sector (2021-2026)*

Source: Debt Management Office Nigeria

Notes:

Exchange rates that were used: 2021- USD/NGN- 403.58, 2022- USD/NGN- 423.75, 2023- USD/NGN- 633.83, 2024- USD/NGN- 1465.04, 2024- USD/JPY- 151.45, 2026- EUR/USD- 1.1699

For loans that run through years like 2015-2023, it is assumed that an equal amount of money is distributed each year

*Find the table at the appendix for reference.

Mining & Construction

Democratic Republic of Congo

The DRC has opened its first gold refining facility in Kalemie. The facility has the capacity to process between 500 – 600 kg of gold per month and is operated by the DRC Gold Refinery S.A. – a partnership between the state-owned DRC Gold Trading S.A. and private firm Lunga Mining.

What this means…

A recurring theme across Africa’s extractive industries is the export of raw materials without fully benefiting from the value chain. The DRC aims to reverse this trend by developing refining capacity in its gold industry. Although the refinery’s capacity only covers about 15.5% of its production, most of which is artisanal, its ability to now produce some quantity of refined gold (up to 99.9% purity) increases the value of its export by 40.6% without an increase in production volume.

Source: DRC Gold Refiner

Fig 2: Approved Loans for the Agricultural Sector (2021-2026)*

Source: Moneda Intelligence

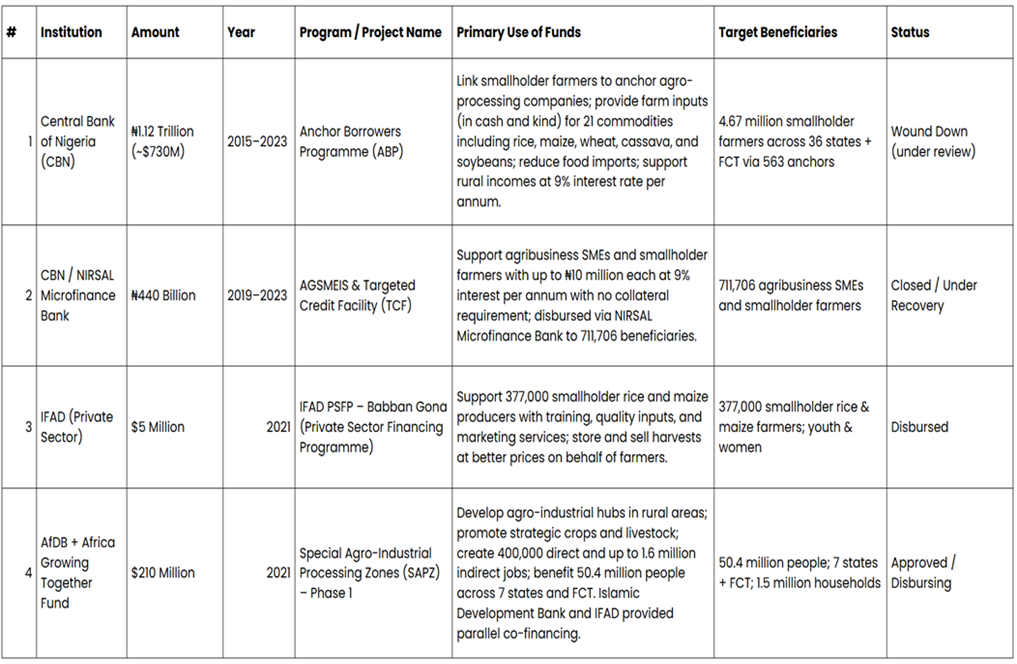

Appendix: Agriculture Sector Loans 2021-2026

Leave a Reply