June 2026

Energy

Algeria

Algeria has commenced construction of its 2,310 km section of the 4,128 km Trans-Sahara Gas Pipeline (TSGP).

Our Thoughts…

This marks the first major construction milestone on one of Africa’s most ambitious cross-border energy infrastructure projects. Estimated to cost between $13 billion and $19.5 billion, the pipeline is designed to transport up to 1.1 trillion cubic feet (Tcf) of natural gas annually, primarily from Warri, Nigeria, through Niger, to Hassi R’Mel, Algeria, where additional gas from Algeria’s domestic fields will be injected into the pipeline. From there, the combined supply will be exported to European markets through Algeria’s existing Mediterranean pipeline network while also supplying natural gas to countries across the Sahel.

The project would establish Nigeria’s first direct pipeline export route to Europe, complementing its existing liquefied natural gas (LNG) exports to the continent, which currently sit at about 314 billion cubic feet (Bcf) annually. At full capacity, the Trans-Sahara Gas Pipeline could more than triple the country’s gas export capacity to the European market.

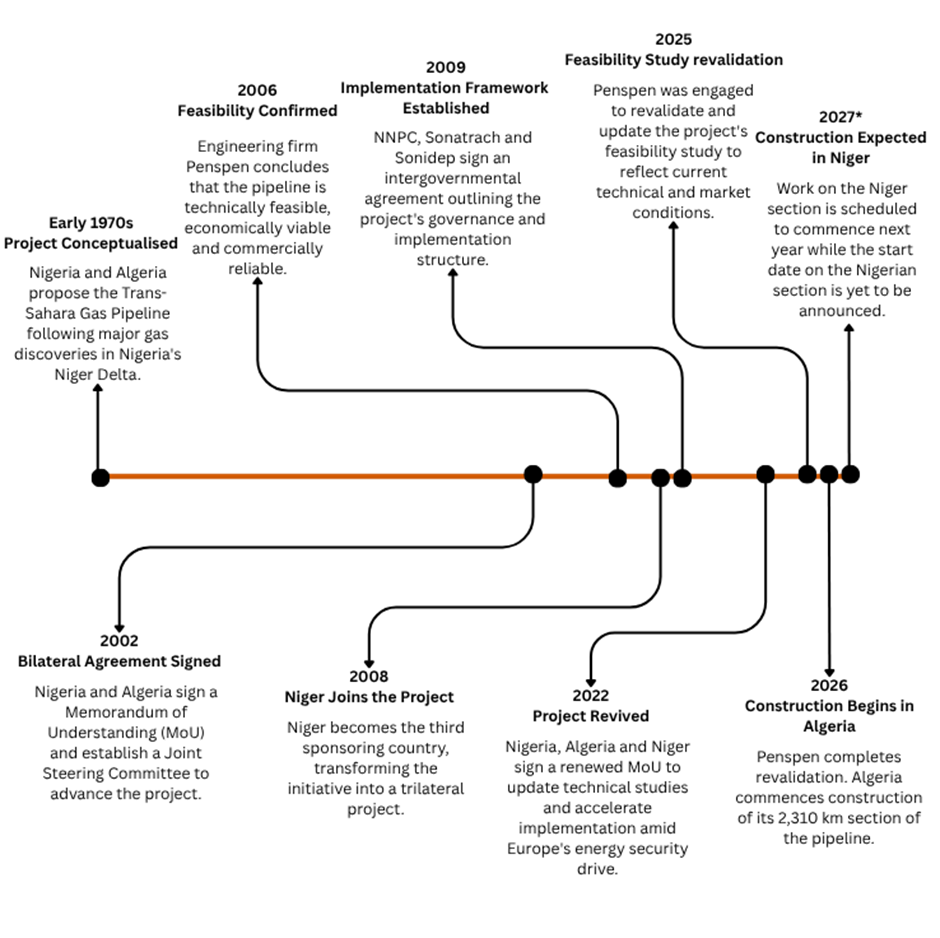

Although first proposed in the early 1970s as a strategic partnership between Nigeria and Algeria to commercialise their abundant natural gas resources, the project made little progress for decades. Momentum only began to build in 2009, when the national oil companies of Nigeria, Algeria and Niger (NNPC Limited, Sonatrach, and Sonidep) signed an intergovernmental agreement that defined the project’s governance framework and technical roadmap, with completion initially scheduled for 2015. The project was subsequently delayed by security concerns, financing constraints, and political instability across sections of the three participating countries.

Interest in the pipeline was reignited in 2022 as Europe accelerated efforts to diversify its gas supplies following Russia’s invasion of Ukraine and the sharp decline in Russian pipeline gas exports. Recognizing an opportunity to position Africa as a strategic alternative supplier, the energy ministers of Nigeria, Algeria and Niger signed a renewed Memorandum of Understanding (MoU) to update technical studies and accelerate implementation. This momentum continued in 2025 with additional agreements to refresh the project’s feasibility studies and implementation framework.

The commencement of construction in Algeria signals that the project is finally moving from decades of planning to execution. For Europe, the pipeline represents another potential source of pipeline gas at a time when energy security and supplier diversification remain strategic priorities. For Nigeria, it provides a long-awaited opportunity to monetize its vast natural gas resources of over 200 Tcf of proven natural gas reserves and an estimated 600 Tcf of additional gas potential.

Beyond exports, the pipeline is expected to strengthen regional energy integration by connecting West and North Africa through shared energy infrastructure while expanding access to natural gas in Niger and other countries along the Sahel corridor. The project also has the potential to stimulate industrial development, improve energy access, and create new opportunities for regional gas trade.

Perhaps most importantly, the start of physical construction in Algeria sends a positive signal to investors that the Trans-Sahara Gas Pipeline is progressing beyond feasibility studies after more than five decades of delays. While significant challenges such as financing the remaining sections, maintaining security along the route and coordinating implementation across three countries remain, the project has now entered a new phase that could transform Africa’s gas export landscape and reinforce the continent’s role in strengthening global energy security.

Source: https://english.news.cn/africa/20260604/d8565688bfe74a7ebfd9aa2e755596c8/c.html

Fig 1: Trans-Sahara Gas Pipeline Project Timeline

Source: Moneda Intelligence

Agriculture

Africa Finance Corporation (AFC) commits $600 million to expand Dangote Fertilizer production across Africa.

What this means…

The Africa Finance Corporation (AFC) has approved a $600 million financing facility for Greenview Fertilizer Corp., Dangote Group’s fertilizer holding company, to support the next phase of its fertilizer expansion programme. The financing forms part of a broader $7 billion investment that will increase the annual urea production capacity of Dangote Fertilizer plant in Nigeria from 3 million metric tonnes per annum (MMTPA) to 9 MMTPA, while also supporting the development of a new 3 MMTPA ureafertilizer plant in Ethiopia. Once completed, the two facilities will have a combined annual production capacity of 12 MMTPA.

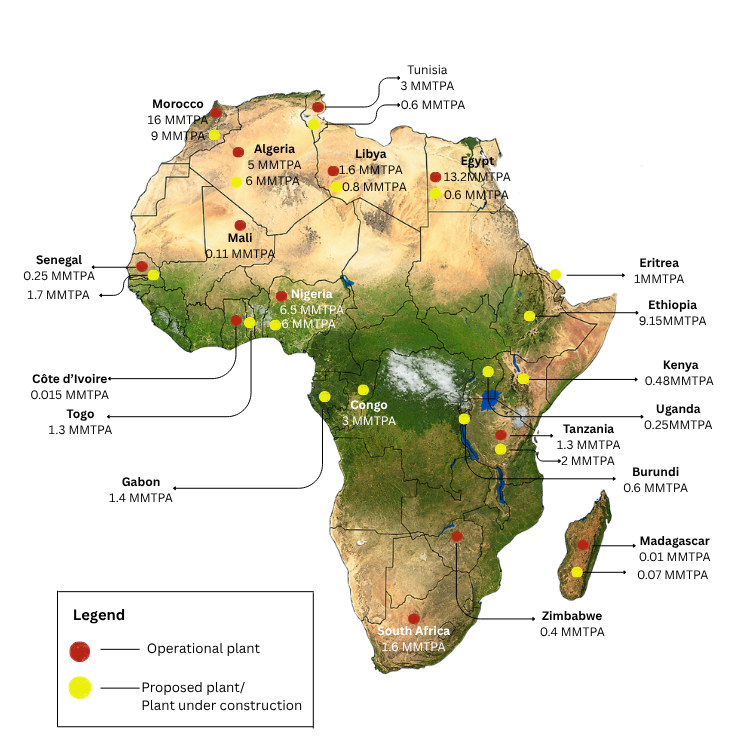

The expansion addresses one of sub-Saharan Africa’s most persistent agricultural challenges: heavy dependence on imported fertilizer despite the region’s abundant natural gas resources. Africa possesses more than 800 trillion cubic feet (Tcf) of proven natural gas reserves, over 70% of which are located in Sub-Saharan Africa. Natural gas is the primary feedstock for urea production, yet the region imports approximately 80% of the fertilizer it consumes, according to the African Development Bank. While North Africa, led by Morocco, Egypt and Algeria, has established itself as a major fertilizer manufacturing and export hub, production capacity south of the Sahara remains limited, exposing farmers to supply disruptions, elevated freight costs, exchange rate volatility and global price shocks.

These vulnerabilities were recently highlighted during disruptions to shipping through the Strait of Hormuz, a key global shipping route that handles approximately one-third of global urea trade and one-quarter of ammonia shipments. The disruption constrained global fertilizer supplies and drove urea prices from approximately $482.50 per tonne on 27 February 2026 to $700 per tonne by 11 March 2026, an increase of about 45% in less than two weeks. For Sub-Saharan African countries that rely heavily on imported fertilizer, such price spikes increase production costs for farmers, reduce fertilizer affordability and application rates, and ultimately weaken agricultural productivity and food security.

Beyond expanding production, the Dangote investment has the potential to reshape Sub-Saharan Africa’s fertilizer market. Upon completion, the project is expected to increase the region’s mineral fertilizer manufacturing capacity by 90%, from approximately 10 MMTPA to 19 MMTPA, significantly improving regional supply security and reducing dependence on imports. Greater availability of locally produced fertilizer could also help increase fertilizer application rates, which currently average only 17- 22.3 kg per hectare (kg/ha) of cropland across Sub-Saharan Africa, compared with the global average of 139 kg/ha. In Central Africa, application rates are estimated to be as low as 8 kg/ha, contributing to some of the continent’s lowest crop yields. By increasing access to affordable fertilizer, the project could help improve agricultural productivity, strengthen food security and increase farmers’ incomes across the region.

Source: https://punchng.com/dangote-afc-sign-600m-deal-for-fertiliser-expansion/

Fig 2: Installed and Proposed Mineral Fertilizer Production Capacity for Selected African Countries

Leave a Reply